Foreign Partnerships in Turkey: Structuring Control, Capital and Exit Rights

Foreign partnership in Turkey is not a single legal form. In practice, it usually means a Turkish company with one or more foreign shareholders, or a joint venture supported by a shareholders' agreement. The legal question is rarely whether a foreigner can invest. In most sectors, the real issue is how the partners divide control, capital obligations, signing power, profit distribution, exit rights, and post-closing compliance from day one.

For international founders, family businesses, and cross-border investors entering the Turkish market, the safest structure is the one that matches the commercial plan before money is committed. A badly drafted partnership can survive the registration phase and still fail later through board deadlock, blocked bank onboarding, unworkable veto rights, or undocumented related-party flows. That is why foreign shareholders in Turkey should treat corporate structuring and shareholder protection as one project, not two separate tasks.

What a Foreign Partnership Usually Looks Like in Turkey

Under the Turkish Foreign Direct Investment framework, foreign investors are generally treated the same as local investors. There is no standalone "foreign partnership company" under Turkish law. Instead, foreign investors typically choose one of the following routes:

- A joint stock company (JSC / A.S.) for investment-heavy or multi-shareholder projects

- A limited liability company (LLC / Ltd.) for closely held operating businesses

- A branch office where the foreign parent wants to remain the main legal center

- A liaison office where no commercial revenue will be generated in Turkey

- An ordinary partnership for limited projects, although this route has no separate legal personality and is rarely the best long-term vehicle for foreign investors

This distinction matters because many disputes begin with a mismatch between business expectations and legal form. A foreign founder may expect equity-style control, while the chosen vehicle only supports a simpler operational partnership. Others register a company quickly and postpone the shareholders' agreement, only to discover later that the articles of association do not protect voting thresholds, transfer restrictions, or exit timing.

Foreign Ownership Rules and Sector Review

For most ordinary commercial activities, 100 percent foreign ownership is possible in Turkey. The usual legal barrier is not nationality itself, but whether the target activity sits in a regulated sector or requires an additional authority review. Official investment guidance specifically flags sectors such as civil aviation, maritime, and broadcasting as examples where sector-specific rules can change the ownership and management analysis.

Before a foreign partnership is signed, the following questions should be answered in writing:

- Does the planned activity require a ministry licence, regulator approval, or professional authorization?

- Is there any shareholding cap, Turkish-citizen requirement, or board composition rule in the sector?

- Will the company operate in free zones, ports, or another location with extra permitting layers?

- Will one of the foreign partners need work authorization to actively manage the business in Turkey?

For investors targeting Izmir, logistics, export, industrial, and services businesses often move quickly from incorporation to operations. That speed is useful only when the legal review happens early. If sector screening is left until after the share split is agreed, fixing the structure later is usually more expensive than getting it right at incorporation.

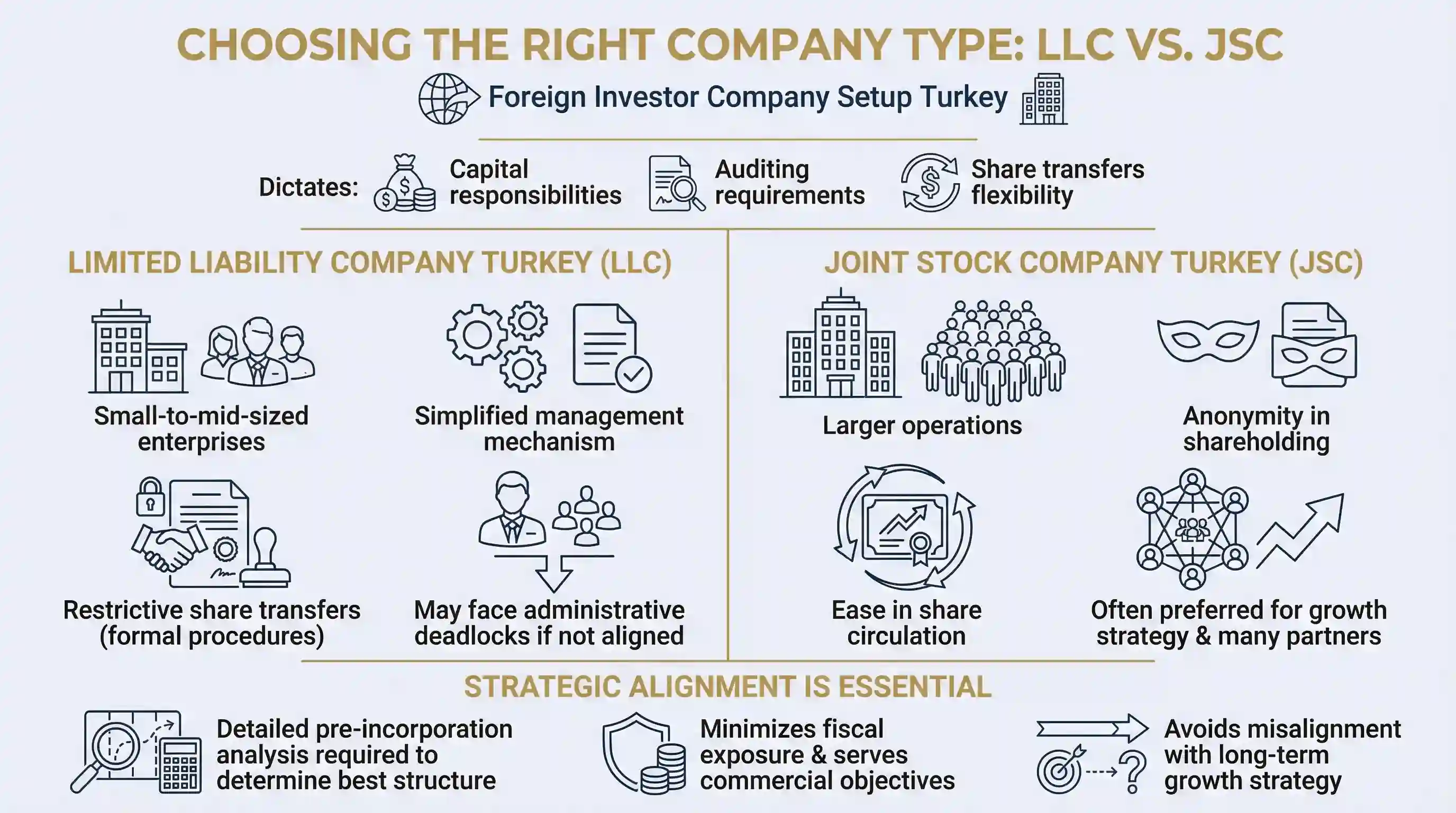

JSC or LLC for a Foreign Joint Venture?

For most foreign shareholders in Turkey, the real choice is between an LLC and a JSC. Both can be used by foreign investors, but they solve different problems.

As of 2026, the statutory minimum capital thresholds are significantly different:

- LLC: TRY 50,000

- JSC: TRY 250,000

The lower LLC threshold makes it attractive for owner-managed businesses and smaller market-entry projects. However, an LLC is usually less flexible when the investors expect future capital rounds, layered control rights, or a cleaner share transfer strategy.

A JSC is often the stronger option when the partnership needs:

- Board-level governance

- Easier transferability of shares

- Different investor classes or differentiated control tools

- Clearer entry and exit planning for multiple investors

- A stronger platform for scaling, acquisition, or institutional investment

An LLC may still be the better fit where:

- The number of partners is small

- The business is operational rather than investment-led

- The shareholders know each other well and want a tighter ownership circle

- The exit horizon is not immediate

The correct choice is not about choosing the "best" company type in the abstract. It is about choosing the form that can actually carry the deal logic the partners negotiated.

The Shareholders' Agreement Is the Real Control Document

Foreign investors often focus on registration steps first and treat the shareholders' agreement as secondary paperwork. In Turkish joint ventures, that is backwards. The registration file creates the company, but the shareholders' agreement usually determines whether the company will remain governable once money, management, and expectations begin to diverge.

A foreign partnership in Turkey should normally settle at least these points before incorporation or closing:

- Capital contribution amounts, timing, and consequences of default

- Board composition and appointment rights

- Reserved matters requiring unanimity or supermajority approval

- Signing authority and banking authority

- Dividend policy and related-party transaction controls

- Non-compete and confidentiality duties

- Pre-emption rights on share sales

- Tag-along and drag-along rights

- Deadlock resolution and forced exit mechanics

- Governing law, dispute forum, and arbitration strategy where appropriate

In our experience, the most expensive disputes are not dramatic fraud cases. They are slower structural failures: one partner controls the company seal, another funds operations informally, a director resigns without a replacement path, or a minority investor discovers that the articles and the side agreement do not work together. A partnership structure is only as strong as the consistency between the company documents, the management model, and the commercial deal.

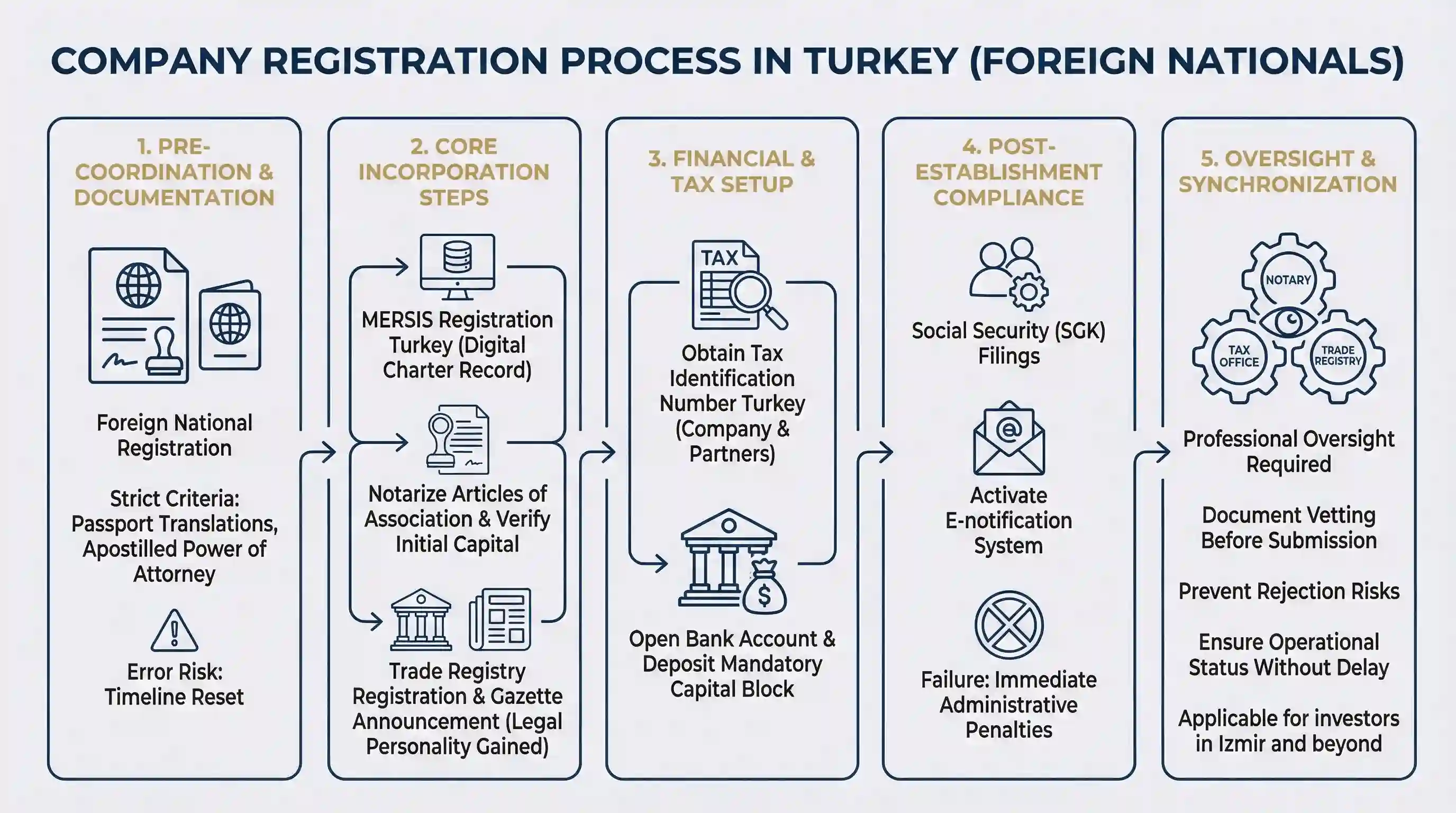

Registration Workflow: MERSIS, Trade Registry and Foreign Documents

Turkey's official investment guidance presents company formation as a one-stop process run through the Trade Registry system, with the memorandum and articles of association submitted through MERSIS. That is directionally true. For a clean domestic file, the registration stage can be fast. In foreign-shareholder matters, however, the real timetable is usually driven by documentation quality.

The practical sequence often includes:

- Confirming the shareholding plan, company type, and management model

- Preparing foreign passports, corporate records, board resolutions, and powers of attorney

- Obtaining apostille or equivalent legalization where required

- Producing Turkish sworn translations and notarizations

- Drafting articles of association consistent with the partnership deal

- Filing through MERSIS and completing Trade Registry steps

- Obtaining tax numbers and completing banking onboarding

- Activating the company for accounting, e-notification, employment, and sector compliance

Most filing delays are not caused by MERSIS itself. They are caused by weak foreign corporate paperwork, unclear signing authority, or documents prepared for another jurisdiction that do not fit Turkish registry practice.

Work Permit and Residence Planning for Foreign Shareholders

Owning shares in a Turkish company does not automatically mean the foreign investor can actively work in Turkey. This point is often missed in cross-border partnerships.

The Ministry of Labour states that work permits are required for foreign persons who will work in the company in roles such as company partner or board member, while certain non-resident JSC board members and non-managing partners may fall within exemption rules. The work-permit analysis should therefore be role-based, not assumption-based.

This distinction matters in three common scenarios:

- A foreign shareholder will live in Turkey and run daily operations

- A foreign shareholder will sign on behalf of the company

- A foreign board appointee will be active in management rather than passive in oversight

Where a work permit is granted, it also functions as a residence basis during its validity. Where the investor will stay in Turkey but not work, the residence strategy must still be planned separately. Mixing up shareholder status, residence status, and work authorization is one of the most common early-stage compliance mistakes in foreign-owned companies.

Banking, Source of Funds and Capital Onboarding

Even when the corporate file is ready, the business is not operational until banking is functional. For foreign-owned companies in Turkey, this is often the point where timelines become unpredictable because banks now examine ownership transparency, source of funds, and commercial rationale much more closely than many investors expect.

Before signing or funding the venture, the partners should clarify:

- Which shareholder will provide the initial funds

- Whether funding enters as paid-in capital, shareholder loan, or future capital commitment

- Which bank will be used and what KYC standards it applies

- Who will hold signing authority on the account

- How cross-border payments to affiliates will be documented

Banking delays are not only practical inconveniences. They can disrupt capital schedules, employee onboarding, supplier contracts, and even the balance of power between shareholders if one side controls the only workable payment route.

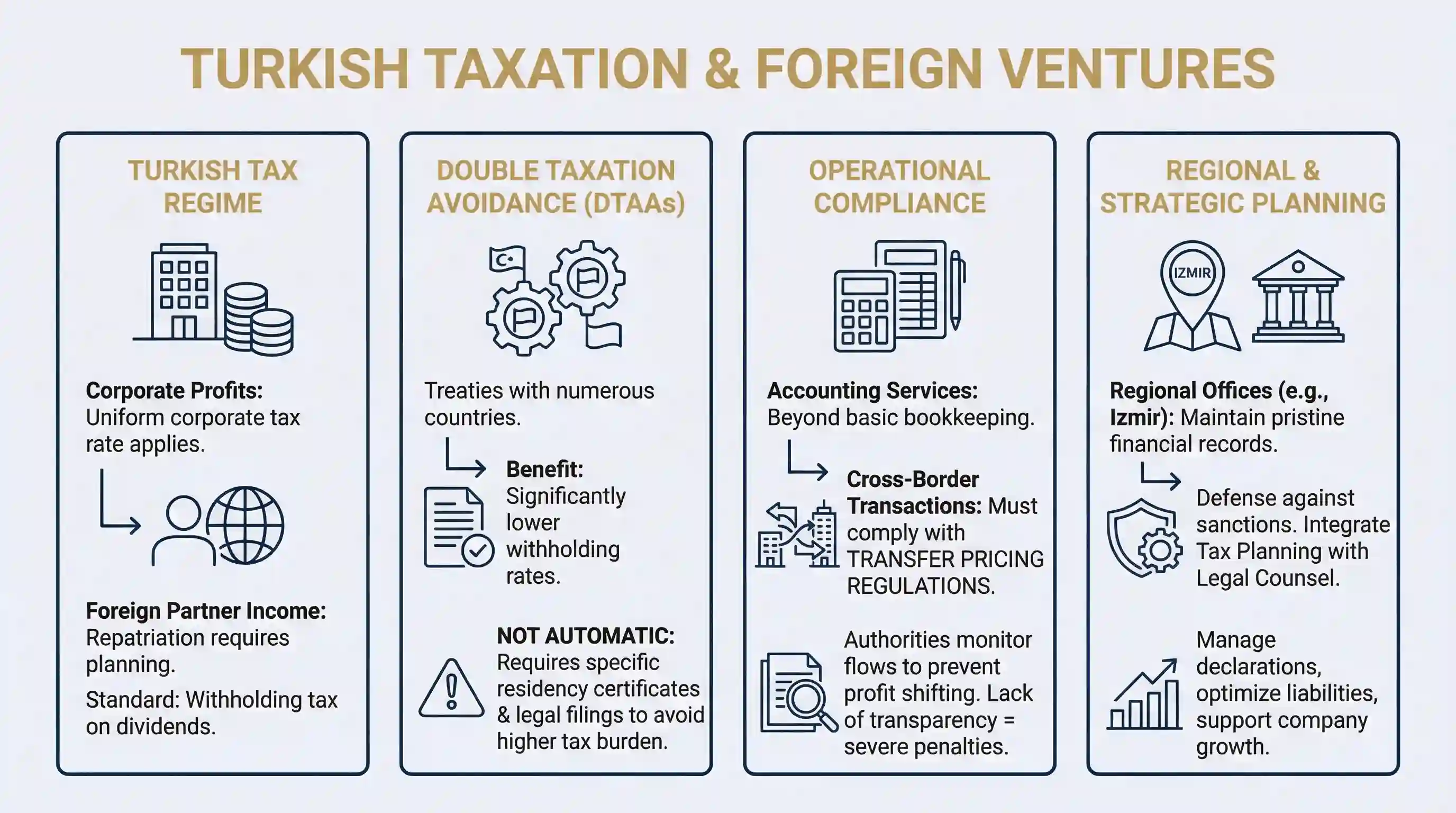

Tax, Profit Repatriation and Ongoing Reporting

Foreign partnerships in Turkey should be designed with post-closing compliance in mind, not just registration in mind. Once the company starts operating, the core issues usually move to bookkeeping discipline, transfer pricing exposure, dividend planning, and regulatory reporting.

Two compliance areas deserve special attention:

1. Cross-border tax planning

Profit extraction should be modeled in advance. Dividends, management fees, royalties, service invoices, and shareholder loans do not create the same tax result. Where a double taxation treaty is relevant, treaty access should be reviewed before distributions are planned, not after funds are ready to leave Turkey.

2. FDI notifications through E-TUYS

For companies and branches within the scope of the foreign direct investment regime, annual and event-based notifications continue after incorporation. Official investment guidance refers to the Activity Information Form, FDI Capital Data Form, and FDI Share Transfer Data Form through the E-TUYS system. In practice, foreign-capital companies should watch the annual May reporting cycle and one-month event-based updates on capital and share changes very carefully.

These obligations are routinely overlooked by investors who assume ordinary accounting compliance is enough. It is not. A foreign-owned company may be fully active commercially and still be out of alignment because its FDI reporting trail is incomplete.

Where Foreign Partnerships Usually Break Down

Most international investors do not need a lecture on why partnerships are risky. They need clarity on where Turkish-market execution tends to go wrong. The most frequent trouble points are:

- a 50/50 structure with no deadlock escape

- a foreign investor funding more than the agreed capital without proper documentation

- unclear authority to sign banking, employment, or lease documents

- related-party services billed without defensible paperwork

- informal promises on future shares that never make it into registered documents

- choosing an LLC when the commercial plan really required JSC-style governance

When these issues surface after a dispute begins, the legal strategy becomes reactive. When they are addressed during structuring, the partnership is usually easier to govern, easier to finance, and easier to exit.

How KL Legal Supports Foreign Partnerships in Turkey

KL Legal advises foreign shareholders, founders, and investor groups on the full legal architecture of entering the Turkish market. That work is not limited to company registration. It includes selecting the right vehicle, aligning the articles with the shareholders' agreement, reviewing management and signature rules, planning work-permit exposure, and reducing later dispute risk.

For clients establishing or expanding operations in Izmir and elsewhere in Turkey, the goal is simple: build a foreign partnership structure that can still function after the first transfer, the first disagreement, the first bank review, and the first compliance deadline.

Frequently Asked Questions

Can a foreigner own 100 percent of a company in Turkey?

Usually yes. In most ordinary sectors, foreign investors can own all shares. The analysis changes in regulated sectors where separate approvals, shareholding limits, or management restrictions may apply.

Is a shareholders' agreement mandatory in Turkey?

Not in every case, but it is strongly recommended in almost every foreign partnership. Without it, key topics such as deadlock, exit, transfer rights, and reserved matters are often left too vague.

Which is better for a joint venture in Turkey: JSC or LLC?

If the project needs layered governance, easier transfer planning, or multiple investor rights, a JSC is often the stronger vehicle. An LLC may still be efficient for smaller, closely held operating businesses.

Do foreign shareholders need a work permit in Turkey?

Share ownership alone is not the full test. If the foreign shareholder or board member will actively work or manage in Turkey, a work-permit assessment is usually required. Passive or non-resident positions can be treated differently.

What filings are often missed after incorporation?

Foreign investors frequently miss E-TUYS notifications, work-permit planning, banking compliance, signature authority alignment, and event-based updates after capital or share changes.